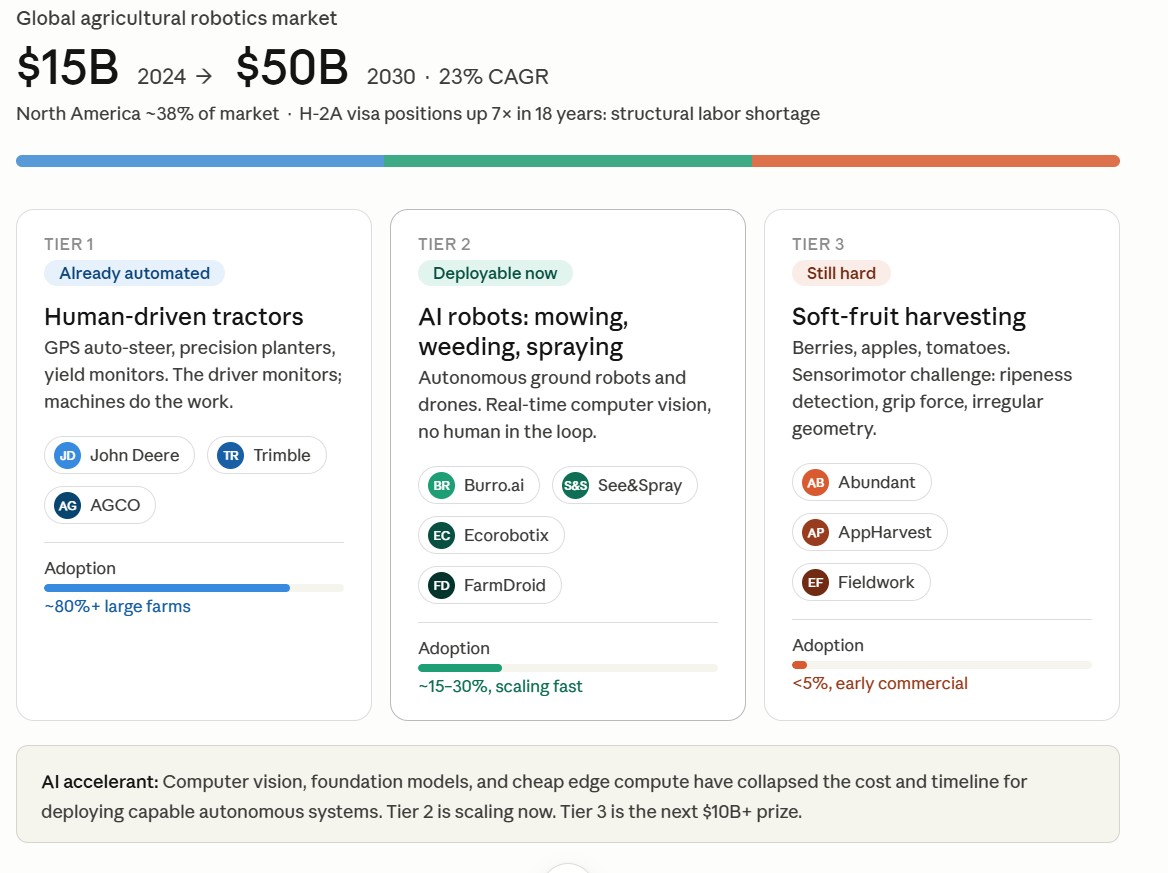

American farmers are facing a structural labor crisis. H-2A temporary ag visa positions have grown more than sevenfold in 18 years, to nearly 385,000 in 2024, and the program has expanded 185% over the past decade alone. This isn’t a cycle. It’s a structural shift — and automation is the answer.

But not all farm tasks automate equally. Think of it as three tiers.

Already done: Row crop farming has been mechanized for decades. GPS-guided, auto-steer tractors have turned fields into precision production systems. The “driver” is more monitor than operator.

Ready now: Mowing, weeding, spraying, soil monitoring. Autonomous robots are commercially deployed and scaling. John Deere’s See & Spray uses computer vision to target individual weeds. Carbon Robotics’ LaserWeeder eliminates weeds with high-powered lasers — no herbicides, no human in the loop. Burro.ai‘s autonomous platform moves through orchards and vineyards, handling transport and canopy work at scale. This layer is real, deployed, and compounding.

Still hard: Strawberries. Blueberries. Apples. Specialty crop sectors remain heavily reliant on seasonal labor because mechanization is still limited in fruit and vegetable harvesting. Identifying ripe fruit, extracting it without bruising, across non-uniform plants — that’s a hard sensorimotor problem. Robots are improving fast, but full automation is still a few years out.

The market reflects the urgency. Agricultural robotics was a $15B market in 2024, projected to reach $50B by 2030.

AI is the accelerant. Computer vision, foundation models, and cheap edge compute have collapsed the cost of building capable autonomous systems. Tasks that required expensive custom engineering five years ago can now be trained from image datasets in months. The key is in the OS and the data. Data is the flywheel that will ultimately provide the moat against new entrants.